Little Swan was once a leader in the industry and a darling of the market. From 1999 to 2000, it held the first place in the domestic washing machine market share for two consecutive years, with a market share of 24% and a cash balance of 1 billion on its books. Seemingly promising with the potential to grow into a new industry giant, Little Swan quickly plummeted to its lowest point in a very short period of time, suffering huge losses for two consecutive years, and was eventually sold to Midea by ST.

What did the little swan experience in just a few years? We interpret the development history of this enterprise and industry from a financial perspective, and seek the common logic behind the rise and fall of the enterprise. What is the financial performance of industry leaders? What is the financial performance that will result in losses?

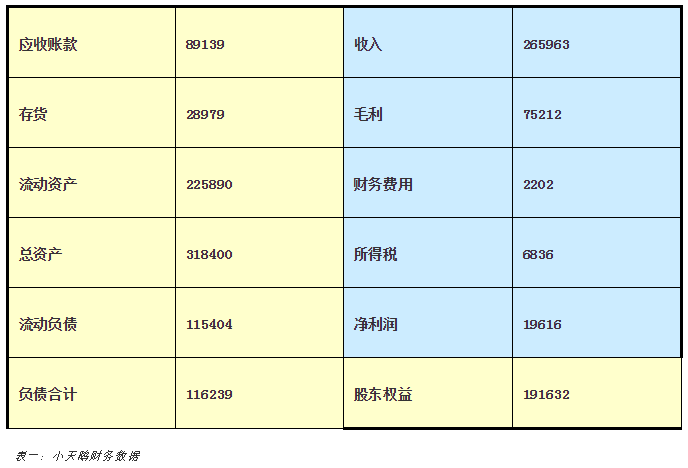

Now back in 1999, Little Swan was the leading player in the washing machine industry, with a market share of 24%. Table 1 shows some data extracted from the financial statements of Little Swan.

QQ screenshot 20190912171518.png

We can analyze the financial performance of Little Swan from three aspects: debt paying ability, operational ability, and profitability. (Students who are familiar with financial indicators can directly jump to Table 2 to see the results):

Let's first take a look at the debt paying ability of the little swan. The indicator for observing the solvency of current liabilities is the current ratio, which is 1.96 when dividing current assets by current liabilities. The ability to repay long-term liabilities includes two aspects: the ability to repay interest and the ability to repay principal. The interest income multiple obtained by dividing pre tax income (net profit+interest+income tax) by financial expenses is 13.

The ability to repay principal depends on the asset liability ratio, also known as financial leverage. The debt to asset ratio obtained by dividing total liabilities by total assets is 37%. Next, let's take a look at Little Swan's operating capacity, mainly various turnover rates.

The total asset turnover rate is obtained by dividing revenue by total assets to obtain 0.84. Divide income by accounts receivable to obtain a accounts receivable turnover rate of 2.98; The turnover rate of inventory is more commonly used to use cost divided by inventory to obtain 6.58.

Let's take a look at profitability again. The most important indicators are gross profit margin and net profit margin. The gross profit margin is divided by revenue, and the net profit margin is divided by revenue, which are 28% and 7.4%, respectively. You can also take a look at the comprehensive profitability of Little Swan. One indicator is the investment return of the entire enterprise, which is the return on total assets. Divide net profit by total assets to obtain 6.16%; Another indicator is the return on investment of shareholders, which is the return on equity. Divide net profit by shareholder equity to obtain 10.24%.

What do these indicator data indicate? We compared Little Swan to Little Duck, a company in the same industry:

It can be seen that the Little Swan has good long-term and short-term debt repayment capabilities, good operational capabilities, and better profitability. It's just a slightly lower gross profit margin.

The business password behind the data

Let's use the previous data to analyze the strategic positioning and business strategy of Little Swan.

The gross profit margin of Little Swan is relatively low, and the turnover rate is relatively high. This indicates that a cost leadership strategy has been adopted. With this strategic positioning, Little Swan has achieved the top market share in the washing machine market for two consecutive years.

How can a cost leadership strategy be considered successful? Of course, it is low-cost and high turnover. So, has the little swan achieved low cost and high turnover? How was it done?

Let's first analyze the cost issue of Little Swan. Have you achieved a lower cost than in the same industry?

In the cost structure of Little Swan, raw material costs account for 90%. Among them, according to the size of the purchase amount, the steel plate is the most purchased. In 2000, there was a severe shortage of steel supply. Buying steel requires approval from the leader. The most important customers of steel plate production enterprises are automobile production enterprises and shipbuilding enterprises. In contrast, Little Swan, which produces washing machines, has a very small purchasing share and no bargaining power at all.

The cost is similar to that of its peers, but it can still increase sales. How did Little Swan achieve this? Selling cheaper than others. The result of doing so is that the duckling has a gross profit of 36%, while the swan only has a gross profit of 28%.

QQ screenshot 20190912171708.png

It is worth noting that although the gross profit margin of the swan is much lower than that of the duckling, its net profit margin is higher than that of the duckling.

The net profit is obtained by subtracting sales, management, and financial expenses from the gross profit. Table 3 shows the proportion of three expenses to revenue for each of the two companies. We see the main difference in financial expenses. Little Swan doesn't need money, borrows very little, and pays very low interest, so financial expenses are very low. The average financial leverage level of Chinese listed companies is 45%, while Little Swan's 37% is definitely a low leverage level.

In addition, the management cost of Little Swan is low, which indicates that with the same income of 100 yuan, Little Swan spends 5 yuan on management and Little Duck spends 11 yuan on management. Little Swan's management efficiency is higher. This makes the profitability of the little swan not poor in the end.

Looking at the operational efficiency of Little Swan, which is the turnover rate, there is no doubt that Little Swan has also performed outstandingly, with the most outstanding being the inventory turnover rate, which is very high. Inventory can be turned over 6.58 times within a year. And the duckling only has 1.53 times. How does a little swan do it?

Because Little Swan adopts an aggressive credit sales strategy. The proportion of accounts receivable to total assets of Little Swan is very high, reaching 29%, while the proportion of inventory is very low, only 2%. The duckling, on the other hand, accounts receivable are 3.1% and inventory is 23%. The financial performance of credit sales is to convert inventory into accounts receivable.

Is converting inventory into accounts receivable a good thing or a bad thing? Being able to retrieve it is a good thing, but not being able to retrieve it becomes a bad thing. There are many benefits to converting inventory into accounts receivable. Selling inventory, seizing the market, avoiding price drops, and many industries have high storage costs for inventory.

However, accounts receivable carry significant financial risks. The turnover rate of accounts receivable for Little Swan is 2.98 times, with an average recovery time of four months. The little duck, who is more conservative in credit sales, does better. This indicates that the Little Swan was right to occupy the market through credit sales at that time.

In addition, the market positioning of Little Swan and Little Duck is also different. In 2000, Xiaoya was the only manufacturer in China that positioned itself as a high-end manufacturer of drum washing machines, with a market share of 5%. Little Swan produces mid to low-end dual cylinder washing machines with a market share of 24%.

Obviously, in 2000, China was still in a relatively early stage of development in the washing machine market. There was more demand for mid to low-end products, which made it easier to sell and thus achieved high turnover rates.

Now, we can summarize the characteristics of Little Swan: adopting a cost leadership strategy, but not truly reducing costs, but adopting a low-priced strategy to capture the market. Due to abundant funds and good management capabilities, the profitability is not poor. At the same time, its low price and aggressive credit sales strategy, as well as its positioning in the mid to low end market, have enabled it to achieve extremely high turnover rates.

Through the above analysis, we have learned what kind of company Little Swan is, but this is not enough. We also need to combine the market environment at that time to see what opportunities and challenges such a company is facing.

At that time, companies in the industry were able to achieve a gross profit margin of over 30%, indicating that competition was not very fierce. But compared to the color TV industry, which belongs to the same household appliances industry, it has been a three-year price war, which makes us realize that the washing machine industry is also on the eve of competition.

In such a market, the cost problem of the little swan cannot be solved in the short term. With the intensification of competition, the financial risk of credit sales will increase. With the adjustment of demand structure, the positioning of the mid to low end market may gradually deviate from market demand. Once sales problems arise, low gross profit margin companies are prone to losses.

Based on this analysis, the prospects of the Little Swan are quite worrying. Everything looks very good, but the crisis is in the near future.

Three strategic transformations

The management of Little Swan is not actually aware of their situation, but as the leading players in this industry, they feel that they should have a sense of crisis and actively consider their future strategic direction.

Little Swan approached a well-known international consulting firm at the time to provide strategic consulting. This consulting company has written a prescription for Little Swan, summarized in one sentence, called "Focusing on washing machines and a concentric diversification strategy.".

The consulting company believes that with the arrival of competition in the washing machine industry, the single business Little Swan is likely to experience a decline in profits and should actively expand its white goods products such as refrigerators and air conditioners. How about expanding the washing machine product line to include dishwashers, dry cleaners, and industrial washing machines? It depends on whether it can cure the disease of the little swan.

The first issue is the cost. Air conditioners and refrigerators also use steel plates, but the amount used is definitely very small at the beginning, and it is also optional for suppliers. The cost still cannot be reduced.

Secondly, the financial risks of aggressive credit sales strategies cannot be resolved by selling refrigerators and air conditioners. In addition, refrigerators and air conditioning cannot solve the positioning problem of washing machines in the mid to low end, and the prescription is not targeted. I have a stomach disease, but the doctor prescribed a medicine for my foot.

Of course, there is also another possibility. The air conditioning and refrigerator business has replaced the declining washing machine business and become the company's new main business in the future. It depends on whether Little Swan has the core ability to make refrigerators and air conditioners.

In the refrigerator and air conditioning industry in 2000, technology was no longer the threshold. The manufacturer combines sales and design. But like most manufacturing companies in China, Little Swan has strong manufacturing capabilities and lacks sales and design capabilities. Unfortunately, Little Swan did not have a correct understanding of itself and began implementing a new strategy in 2001.

In the following five years, the sales of Little Swan's main business remained stable, while sales revenue significantly declined. This indicates a fierce price war. In 2003, the gross profit was two billion less than in 2000:

QQ screenshot 20190912171804. png

The air conditioning business suffered a complete loss. The refrigerator business is not much better. The quantity is very small and cannot be scaled up. It cannot completely compensate for the loss of the washing machine. It should be said that Little Swan's strategic transformation has been very effective. Strategic transformation was carried out in 2000, and losses occurred in 2001. Losses continued in 2002. The loss amount reached 560 million, and the credit sales strategy caused significant financial losses. In 2001, a bad debt provision of 107 million was made, compared to 329 million in 2002. During the period from 2001 to 2006, a total of 1.778 billion yuan of bad debt provisions were made, and 1.226 billion yuan of bad debt provisions were made for other receivables. It is obvious that bad debts caused the loss.

Due to two consecutive years of losses, Little Swan was specially treated and became ST Little Swan.

Faced with the failure of its first strategic transformation, Little Swan launched its second strategic transformation in 2005, which was to do OEM work for international brands such as General Electric and Hitachi Electric. OEM does not need to be responsible for product design and sales, only for production and manufacturing. Although it may not earn much money, it is suitable for Little Swan.

In 2007, Little Swan's performance saw a rapid growth, with a profit margin of 7%. This is the profit margin indicator used by Little Swan as the leader of the washing machine industry back then. After a full eight years, it has returned to its starting point.

But then Little Swan made its third major strategic adjustment and sold itself to Midea. Because the competition in the washing machine industry has entered a white hot stage, it has fallen into a situation where almost the entire industry is losing money.

Midea is a company with unique advantages in sales and design. Acquiring Little Swan, which excels in manufacturing, is a complementary advantage. In fact, after being acquired by Midea, Little Swan has maintained very good performance, with a net profit margin of around 8% in recent years.

Although Little Swan is still an excellent enterprise in the home appliance industry today, it could have independently become the leader of this industry. Looking back at this period of history, while regretful, I hope it can also bring you some thoughts and insights.

{kind=link}